Yahoo Finance

Yahoo Finance Earnings Not Telling The Story For HML Holdings plc (LON:HMLH)

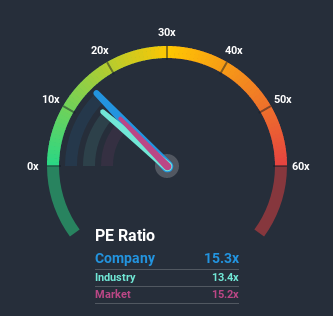

It's not a stretch to say that HML Holdings plc's (LON:HMLH) price-to-earnings (or "P/E") ratio of 15.3x right now seems quite "middle-of-the-road" compared to the market in the United Kingdom, where the median P/E ratio is around 15x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

While the market has experienced earnings growth lately, HML Holdings' earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for HML Holdings

Want the full picture on analyst estimates for the company? Then our free report on HML Holdings will help you uncover what's on the horizon.

Is There Some Growth For HML Holdings?

In order to justify its P/E ratio, HML Holdings would need to produce growth that's similar to the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 21%. This means it has also seen a slide in earnings over the longer-term as EPS is down 7.1% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next year should bring plunging returns, with earnings decreasing 108% as estimated by the lone analyst watching the company. Meanwhile, the broader market is forecast to moderate by 11%, which indicates the company should perform poorly indeed.

In light of this, it's somewhat peculiar that HML Holdings' P/E sits in line with the majority of other companies. When earnings shrink rapidly the P/E often shrinks too, which could set up shareholders for future disappointment. There's potential for the P/E to fall to lower levels if the company doesn't improve its profitability.

The Key Takeaway

The price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that HML Holdings currently trades on a higher than expected P/E since its earnings forecast is even worse than the struggling market. When we see a weak earnings outlook, we suspect the share price is at risk of declining, sending the moderate P/E lower. We're also cautious about the company's ability to resist even greater pain to its business from the broader market turmoil. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

There are also other vital risk factors to consider before investing and we've discovered 2 warning signs for HML Holdings that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies that have grown earnings strongly and trade on P/E's below 20x.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.