Yahoo Finance

Yahoo Finance The Estee Lauder Companies (EL) Online Business Aids Growth

The Estee Lauder Companies Inc. EL has a strong e-commerce business, which is proving to be a major growth engine. Strength in the company’s Skin Care business is also an upside. The leading skin care, makeup, fragrance and hair care product provider’s solid presence in emerging markets is noteworthy.

Let’s delve deeper.

Image Source: Zacks Investment Research

Factors Working Well for The Estee Lauder Companies

The company’s online operations have been working well for some time now. The Estee Lauder Companies has been implementing new technology and digital experiences, including online booking for each store appointment, omnichannel loyalty programs and high-touch mobile services. These initiatives and the company’s digital-first mindset have been aiding its online sales. EL is expanding its omnichannel capabilities to provide flexible and convenient shopping options to consumers.

The Zacks Rank #3 (Hold) company’s Skin Care portfolio has been performing well. During the third quarter of fiscal 2022, the Skin Care category’s sales were up 6% year over year (up 7% at constant currency or cc) to $2,395 million. In May 2021, The Estee Lauder Companies took a step to expand its Skin Care business when it concluded the first phase of raising its ownership stake in DECIEM Beauty Group Inc. (DECIEM). The Estee Lauder Companies now has nearly 76% ownership in DECIEM compared with 29% earlier. The addition of DECIEM complimented the company’s reported sales growth in the fiscal third quarter.

The company has a strong presence in emerging markets, insulating it from the macroeconomic headwinds in the matured markets. The company derives significant revenues from emerging markets like Thailand, India, Russia and Brazil, encouraging it to make distributional, digital and marketing investments in these countries. The Estee Lauder Companies is investing to cater to consumer demand in China and Asia. To this end, it bought Korea-based skincare brand Dr. Jart in 2019.

Is All Rosy For The Estee Lauder Companies?

During the third quarter of fiscal 2022, The Estee Lauder Companies’ organic sales fell in mid-single-digits across Mainland China, as online growth was offset by a heavy decline in brick-and-mortar sales. The company witnessed increased pandemic-inflicted restrictions across China from March 2022. Such temporary restrictions caused softness in consumer traffic and travel. In its last earnings call, management said that although it believes that the ongoing restrictions in China are temporary, it expects these headwinds to have a greater impact on fourth-quarter results relative to the third quarter.

Although the company’s fiscal 2022 guidance reflects year-over-year growth, it has been recently downgraded from the previous forecast. Management revised its fiscal 2022 outlook downward as impressive performance is likely to be countered with added headwinds that are affecting the fiscal fourth-quarter view. These headwinds include pandemic-induced restrictions in China, impacting travel retail business. Also, the invasion of Ukraine is a major hurdle. For fiscal 2022, the company projects reported net sales to increase in the band of 7-9% year over year. The metric was expected to increase 13-16% year over year. The company expects adjusted earnings per share (EPS) between $7.05 and $7.15 for fiscal 2022, compared with the previous range of $7.43-$7.58. Adjusted earnings are anticipated to increase 8-10% at cc in fiscal 2022. Earlier, the metric was projected to increase 14-17% at cc.

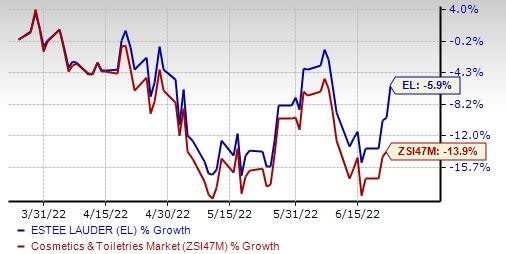

That said, focus on the aforementioned upsides is likely to offer some respite. Shares of EL have dropped 5.9% in the past three months compared with the industry’s 13.9% decline.

Looking for Better-Ranked Staple Bets? Check These

Some better-ranked stocks are Pilgrim’s Pride PPC, Sysco Corporation SYY and United Natural Foods UNFI.

Pilgrim’s Pride, which produces, processes, markets and distributes fresh, frozen and value-added chicken and pork products, sports a Zacks Rank #1 (Strong Buy). PPC has a trailing four-quarter earnings surprise of 31.4%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Pilgrim’s Pride’s current financial year EPS suggests growth of 63.2% from the year-ago reported number.

Sysco, which engages in marketing and distributing various food and related products, sports a Zacks Rank #1. SYY has a trailing four-quarter earnings surprise of 9.1%, on average.

The Zacks Consensus Estimate for Sysco’s current financial year sales and EPS suggests growth of 32.6% and 124.3%, respectively, from the year-ago reported number.

United Natural Foods distributes natural, organic, specialty, produce and conventional grocery and non-food products. UNFI currently sports a Zacks Rank #1.

The Zacks Consensus Estimate for UNFI’s current financial year sales and EPS suggests growth of 7.2% and 4.9%, respectively, from the year-ago period’s reported figures. United Natural Foods has a trailing four-quarter earnings surprise of 29.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

To read this article on Zacks.com click here.

Zacks Investment Research