Yahoo Finance

Yahoo Finance Here's Why You Should Hold on to Stryker (SYK) Stock for Now

Stryker Corporation SYK is well-poised for growth, backed by a robust robotic-arm assisted surgery platform, Mako, and a diversified product portfolio. However, pricing pressure remains a headwind.

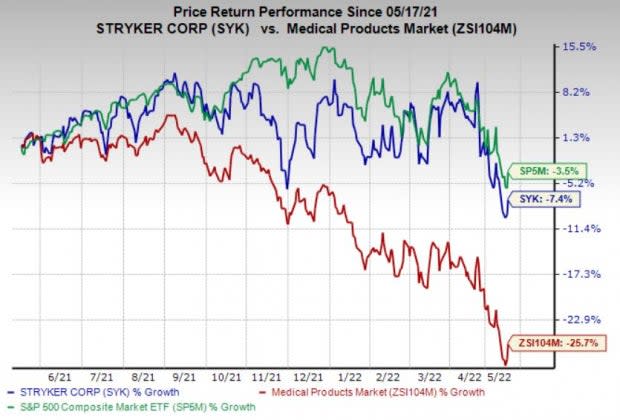

Shares of the Zacks Rank #3 (Hold) company have lost 7.4% compared with the industry’s decline of 25.7% in a year’s time. The S&P 500 Index has fallen 3.5% in the same time frame.

Stryker, with a market capitalization of $88.21 billion, is one of the world’s largest medical device companies operating in the orthopedic market. It anticipates earnings to improve 9.2% in the next five years. Stryker’s earnings yield of 4.1% compares favorably with the industry’s 0.7%.

What’s Favoring Growth?

The company continues to witness strong demand for Mako and a healthy order book, courtesy of the platform’s unique features despite financial constraints stemming from the COVID-19 pandemic. This, in turn, positions it well to sustain momentum in robot sales and recon share market gains.

The company is committed to the continued expansion of Mako. In 2021, the company’s Mako installed base saw growth of 27%, and currently has an installed base that is moving toward 1500 Mako robots. Thus, the company continues to focus on the continued expansion of the platform. This growth reflects the demand for Stryker’s differentiated Mako robotic technology.

Taking into account the normalization of the customer environment, management anticipates another strong year for Mako in 2022. Hence, for 2022, the company’s Mako order book remains solid and is in sync with its aim of continued share gains in both hips and knees.

Image Source: Zacks Investment Research

Additionally, Stryker has a diversified product portfolio. Its wide range of products shields the company against any significant sales shortfall during economic turmoil. Its significant exposure in robotics, Artificial Intelligence for health care and Medical Mechatronics has helped the company stay ahead of the curve in the MedTech space. Stryker’s portfolio includes products like Hip, Knee and Mako robotic-arm assisted surgeries.

In September 2021, the company’s Trauma & Extremities division introduced a Citrelock Tendon Fixation Device System, which offers surgeons a differentiated design through a tendon thread featuring Citregen — a resorbable technology. Citregen, in particular, has chemical and mechanical qualities intended for orthopedic surgical applications.

Per management, the company’s sustained support for customers and focus on innovation poise it for growth as the pandemic eventually subsides. In the first quarter of 2022, Stryker’s adjusted R&D expenses were 7.2% of net sales, highlighting its sustained commitment to innovation. Per management, this is likely to drive new product launches.

What’s Hurting the Stock?

An unfavorable pricing environment poses a persistent threat to Stryker’s core businesses. Per the first-quarter 2022 earnings call, the period’s average selling days were in line with first-quarter 2021. The impact from pricing was 1% in the last reported quarter. Consequently, pricing pressure remains a cause of concern.

Estimate Trend

The Zacks Consensus Estimate for 2022 earnings per share is pegged at $9.64, suggesting growth of 6.1% from 2021. The consensus mark for 2022 revenues stands at $18.43 billion, indicating an improvement of 7.7% from the previous year.

Stocks to Consider

Some better-ranked stocks in the broader medical space are AMN Healthcare Services, Inc. AMN, Masimo Corporation MASI and Veeva Systems, Inc. VEEV.

AMN Healthcare surpassed earnings estimates in each of the trailing four quarters, the average surprise being 15.6%. The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

AMN Healthcare’s long-term earnings growth rate is estimated at 1.1%. The company’s earnings yield of 11.4% compares favorably with the industry’s (0.8%).

Masimo beat earnings estimates in each of the trailing four quarters, the average surprise being 4.4%. The company currently carries a Zacks Rank #2 (Buy).

Masimo’s estimated earnings growth rate for second-quarter 2022 is pegged at 22.3%. The company’s earnings yield is pegged at 3.8% against the industry’s (8.5%).

Veeva Systems surpassed earnings estimates in each of the trailing four quarters, the average surprise being 9.6%. The company currently carries a Zacks Rank #2.

Veeva Systems’ long-term earnings growth rate is estimated at 18.1%. The company’s earnings yield of 2.4% compares favorably with the industry’s 0.2%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Stryker Corporation (SYK) : Free Stock Analysis Report

Masimo Corporation (MASI) : Free Stock Analysis Report

AMN Healthcare Services Inc (AMN) : Free Stock Analysis Report

Veeva Systems Inc. (VEEV) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research