Yahoo Finance

Yahoo Finance Here's Why Investors Should Retain Dover (DOV) Stock For Now

Dover Corporation DOV is gaining from forecast-beating earnings in second-quarter 2022. Solid end-market demand across all segments, bookings rates and robust order backlog are aiding growth. Benefits from cost-reduction actions, productivity gains, focus on investments and acquisitions and efforts to reduce debt levels will continue to drive results.

Earnings Surpass Q2 Estimates: Dover’s second-quarter 2022 earnings beat the respective Zacks Consensus Estimate and increased year over year.

Positive Earnings Surprise History: Dover, a Zacks Rank #3 (Hold) company, has a trailing four-quarter earnings surprise of 5.1%, on average.

Return on Equity (ROE): Dover’s trailing 12-month ROE of 26.9% emphasizes its growth potential. The company’s ROE is higher than the industry’s ROE of 23.6%, highlighting its efficiency in utilizing shareholders’ funds.

Underpriced: Looking at the price-to-earnings ratio, Dover’s shares are underpriced at the current level, which is attractive for investors. The company has a trailing P/E ratio of 16.9, below the industry average of 20.8.

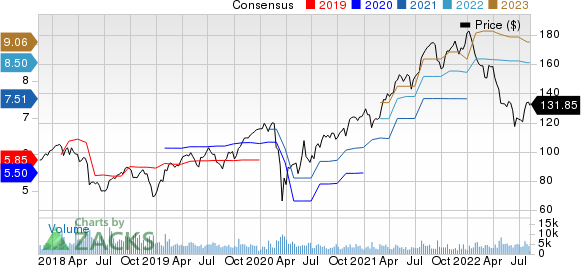

Positive Growth Expectations: The company’s earnings estimate for the current year is pegged at $8.50, suggesting year-over-year growth of 11.4%.

Other Growth Drivers

Dover has been gaining from robust order trends across most of its businesses for a while, stemming from strong end-market demand. The company is well poised to deliver robust top-line growth, margin expansion and double-digit earnings per share (EPS) growth in 2022, driven by a strong backlog, margin conversion efforts, benefits from acquisitions, capacity expansion investments and productivity improvement. DOV expects adjusted EPS to be between $8.45 and $8.65 for 2022, up from $7.63 per share reported in 2021. Organic revenue growth is expected between 8-10% for 2022. Also, the company’s productivity and cost-control initiatives will continue to drive bottom-line growth.

In the Engineered Products segment, demand for engineered products, vehicle service and industrial automation has been solid. A solid backlog and strong bookings will continue to support the segment’s top line. Orders for refuse trucks and software solutions remain robust, with new order rates pushing well into the year’s second half. The Clean Energy and Fueling segment will gain from solid growth in below-ground retail fueling, fuel transport vehicle wash and industrial gases and acquisitions in Clean Energy and components.

The Imaging & Identification segment will gain from the recovery in component shortages from second-quarter COVID shutdowns in China, with demand improvement in textiles. In the Pumps & Process Solutions segment, industrial pumps and polymer processing activity remains solid and precision components continue their upward growth trajectory in bearings and compressor components.

Given the large backlog and pricing initiatives, the Climate and Sustainability Technologies segment will perform well in 2022. Demand remains robust across all lines in food retail. Food retail shipments are expected to improve in the second half of the year. Also, its heat exchanger and beverage packaging business are seeing strong order rates and a record backlog for high-efficiency heat pumps. Margins across all the segments will improve in the second half of 2022, owing to improved price/cost, volume growth, productivity gains and favorable product and business mix.

Dover invests in capacity expansions in high-growth businesses and productivity improvements across its portfolio. Dover has a long tradition of making successful acquisitions in diverse end markets. The company recently completed the Malema buyout, which has now become part of the PSG business unit within Dover's Pumps & Process Solutions segment. The acquisition will expand the company’s biopharma single-use production offering. Dover will remain active on the buyout front in the current year. This April, Dover acquired certain intellectual property associated with electrically-operated refuse collection vehicle bodies from Boivin Evolution Inc. The buyout will expand the technological footprint and product portfolio of Dover’s Environmental Solutions Group business unit within its Engineered Products segment.

The company’s efforts to reduce debt levels, its solid financial position, prudent capital structure, refinancing efforts and momentum in operational execution bode well.

Material cost inflation, input shortages, COVID-19 Omicron variant-related absenteeism and supply chain challenges and labor constraints will continue to affect the company’s margin performance.

Dover Corporation Price and Consensus

Dover Corporation price-consensus-chart | Dover Corporation Quote

Stocks to Consider

Some better-ranked stocks from the Industrial Products sector are Greif Inc. GEF, Titan International TWI and MRC Global MRC. All of these stocks sport a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Greif has an estimated earnings growth rate of 37% for the current year. In the past 60 days, the Zacks Consensus Estimate for current-year earnings has been revised upward by 17%.

Greif pulled off a trailing four-quarter earnings surprise of 22.9%, on average. GEF’s shares have risen 17% in the past year.

Titan International has an estimated earnings growth rate of 165% for the current year. In the past 60 days, the Zacks Consensus Estimate for current-year earnings has been revised upward by 43%.

Titan International pulled off a trailing four-quarter earnings surprise of 56.4%, on average. TWI’s shares have soared 101% in a year.

MRC Global has an expected earnings growth rate of 259% for 2022. The Zacks Consensus Estimate for the current year’s earnings moved up 24% in the past 60 days.

MRC Global has a trailing four-quarter earnings surprise of 140.8%, on average. MRC’s shares have surged 35% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dover Corporation (DOV) : Free Stock Analysis Report

Titan International, Inc. (TWI) : Free Stock Analysis Report

Greif, Inc. (GEF) : Free Stock Analysis Report

MRC Global Inc. (MRC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research