Yahoo Finance

Yahoo Finance Here's Why Investors Should Retain Thermo Fisher (TMO) Stock

Thermo Fisher Scientific Inc. TMO is well-poised to grow in the coming quarters, backed by the promising strength of its businesses in end markets. The company’s series of strategic buyouts is also likely to propel future growth. Strong solvency also buoys optimism. However, the downturn in COVID-19 testing demand and macroeconomic headwinds remain concerns for the stock.

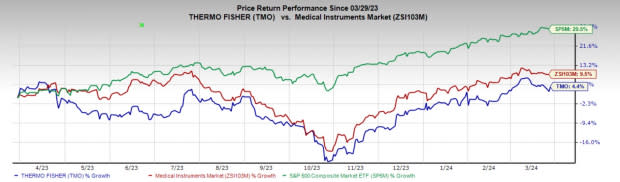

In the past year, this Zacks Rank #3 (Hold) stock has increased 4.4% compared with the 9.5% rise of the industry and a 29.5% increase of the S&P 500 composite.

The renowned medical and laboratory equipment provider has a market capitalization of $216.90 billion. TMO has an earnings yield of 3.78% against the industry’s -6.34%. In the last reported quarter, the company delivered an earnings surprise of 0.53%.

Let’s delve deeper.

Upsides

Strength in End Markets: Within the pharma and biotech end market, of late, Thermo Fisher’s biosciences and bioproduction businesses have significantly expanded their capacity to meet global vaccine manufacturing requirements. The pharma services business has been providing services to the pharma and biotech customers, which they need to develop and produce vaccines and therapies globally.

In terms of the latest update, within the end market, the academic and government business grew in the mid-single digits in the fourth quarter of 2023. The company delivered strong growth across a range of its businesses during the year, including electron microscopy, chromatography and mass spectrometry, as well as the research and safety market channel. In industrial and applied, Thermo Fisher grew in the low single digits.

Image Source: Zacks Investment Research

Strategic Acquisitions to Boost Growth: Thermo Fisher’s business strategy primarily includes expansion through the strategic acquisition of technologies and businesses that augment the company’s existing products and services. In October 2023, the company announced its plan to acquire Olink Holdings, whose highly differentiated solutions will enhance Thermo Fisher’s capabilities in the high-growth proteomics market.

Thermo Fisher’s acquisition of CorEvitas advanced its clinical research capabilities with a leading regulatory-grade registry platform. The addition of MarqMetrix is a strategic fit for the company as it adds highly complementary Raman-based in-line PAT to the portfolio. Further, TMO acquired The Binding Site, expanding its existing specialty diagnostics portfolio with the latter’s pioneering innovation in diagnostics and monitoring for multiple myeloma.

Stable Solvency: Thermo Fisher ended 2023 with no debt on its balance sheet, which looks promising. The company had cash and cash equivalents of $8.08 billion in 2023 compared with $8.52 billion at the end of 2022.

The times interest earned for the company stands at 5.6%, a sequential decline from 6.1% at the end of the third quarter of 2023.

Downsides

Lower COVID-19 Sales Hurt Growth: During the COVID-19 public health emergency, Thermo Fisher’s biosciences and bioproduction businesses expanded their capacity to meet the global vaccine manufacturing requirements of pharma and biotech customers. However, since the past few quarters, Thermo Fisher has been experiencing a continuous decline in COVID-19 testing-related demand. During 2023, sales growth in all major regions declined due to decreased demand for COVID-19-related products.

Macroeconomic Challenges Continue to Weigh on TMO: The challenging macroeconomic scenario and slower economic recovery in China continue to hurt Thermo Fisher's growth. The company has been witnessing headwinds in the government and academic markets. Moreover, many countries in Europe are also going through a tough time that might impact their academic budgets. In the fourth quarter of 2023, North America declined in the low double digits, and Europe declined in the low single digits.

Estimate Trend

The Zacks Consensus Estimate for the company’s 2024 earnings per share (EPS) has moved up from $21.52 to $21.53 in the past 30 days.

The Zacks Consensus Estimate for TMO’s 2024 revenues is pegged at $42.74 billion. This suggests a 0.3% drop from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Cardinal Health CAH, Stryker SYK and DaVita DVA.

Cardinal Health has a long-term estimated earnings growth rate of 14.2% compared with the industry’s 11.6%. CAH’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 15.6%. Its shares have increased 50.9% compared with the industry’s 14.2% rise in the past year.

CAH carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Stryker, carrying a Zacks Rank #2 at present, has an earnings yield of 3.36% compared to the industry’s 0.02%. Shares of the company have increased 28.5% compared with the industry’s 5.2% rise over the past year.

SYK’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 5.2%. In the last reported quarter, it delivered an average earnings surprise of 5.81%.

DaVita, sporting a Zacks Rank #1 at present, has an estimated long-term earnings growth rate of 12.1% compared with the industry’s 11.9%. Shares of DVA have rallied 74.4% compared with the industry’s 22% rise over the past year.

DVA’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 35.6%. In the last reported quarter, it delivered an average earnings surprise of 22.2%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Stryker Corporation (SYK) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report

Thermo Fisher Scientific Inc. (TMO) : Free Stock Analysis Report

Cardinal Health, Inc. (CAH) : Free Stock Analysis Report