Yahoo Finance

Yahoo Finance Here's Why You Should Retain Masimo (MASI) Stock For Now

Masimo Corporation MASI is well poised for growth in the coming quarters, backed by its slew of favorable study outcomes over the past few months. A robust third-quarter 2021 performance, along with its focus on patient monitoring, is expected to contribute further. However, concerns regarding overdependence on Masimo SET and forex woes persist.

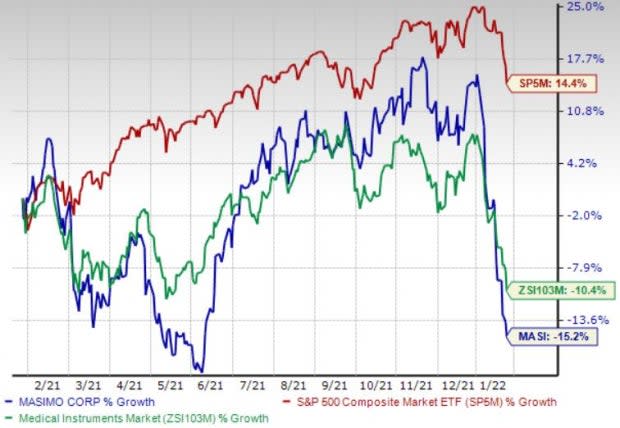

Over the past year, this Zacks Rank #3 (Hold) stock has lost 15.2% compared with 10.4% fall of the industry. The S&P 500 has risen 14.4% in the same time frame.

The renowned global provider of non-invasive monitoring systems has a market capitalization of $12.03 billion. The company projects 11.6% growth for 2022 and expects to maintain its strong performance. Masimo has delivered an earnings surprise of 5.38% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Positive Study Outcomes: We are optimistic about Masimo’s products, which have been subjects of various studies over the past few months. The company, in December 2021, announced the findings of a favorable study result wherein researchers evaluated the relationship between parameters derived from electroencephalogram (“EEG”) spectra and postoperative delirium in older patients undergoing elective surgery. The EEG spectra was measured using Masimo SedLine Brain Function Monitoring.

In November, Masimo announced the findings of a study, demonstrating the experience of using the Masimo Rad-G Pulse Oximeter. The study evaluated that Rad-G Pulse Oximeter supports health providers in detecting and managing pneumonia in children aged less than five years with symptoms of acute respiratory infection.

Patient-Monitoring in Focus: Masimo, during its third-quarter 2021 earnings call in October, confirmed that it had recorded strong demand from hospitals for its monitors, especially the SET pulse oximeters and rainbow Pulse CO-Oximeters. The company’s recurring revenue stream of single-patient-use sensors has also increased significantly over the past two years on the back of new customer wins, increased utilization across its installed base and the expansion of patient monitoring in hospitals, thus raising our optimism.

Strong Q3 Results: Masimo’s solid third-quarter 2021 results buoy our optimism. The company recorded a strong rebound in sensor sales (on the back of steady expansion of monitoring in hospitals), along with robust order shipments, which is encouraging. Expansion of the company’s installed base is also impressive. A slew of regulatory approvals raises our optimism. Product launches over the past few months is also impressive. Expansion of both margins bodes well for the stock. A raised financial outlook for 2021 augurs well.

Downsides

Overdependence on Masimo SET: Masimo currently derives the majority of its revenues from its primary product offerings like the Masimo SET platform, Masimo rainbow SET platform and related products. Thus, the company’s business is highly dependent upon the continued success and market acceptance of its primary product offerings.

Forex Woes: Masimo markets its products in certain foreign markets through its subsidiaries and other international distributors. As a result, events that result in global economic uncertainties could significantly affect its results of operations in the form of gains and losses on foreign currency transactions, and potential devaluation of the local currencies of Masimo’s customers relative to the U.S. dollar.

Estimate Trend

Masimo is witnessing a negative estimate revision trend for 2022. In the past 90 days, the Zacks Consensus Estimate for its earnings per share has moved 2.7% south to $4.33.

The Zacks Consensus Estimate for the company’s fourth-quarter 2021 revenues is pegged at $319.2 million, suggesting an 8.2% improvement from the year-ago quarter’s reported number.

Key Picks

A few stocks from the broader medical space that investors can consider are AMN Healthcare Services, Inc. AMN, Cerner Corporation CERN and Catalent, Inc. CTLT.

AMN Healthcare has an estimated long-term growth rate of 16.2%. AMN’s earnings surpassed estimates in the trailing four quarters, the average surprise being 19.51%. It currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

AMN Healthcare has gained 23.8% against the industry’s 62.1% fall over the past year.

Cerner, carrying a Zacks Rank #2 (Buy), has an estimated long-term growth rate of 12.8%. CERN’s earnings surpassed estimates in three of the trailing four quarters, the average surprise being 3.21%.

Cerner has gained 13.9% against the industry’s 57.2% fall over the past year.

Catalent has an estimated long-term growth rate of 16.9%. CTLT’s earnings surpassed estimates in the trailing four quarters, the average surprise being 9.88%. It currently carries a Zacks Rank #2.

Catalent has lost 11.8% compared with the industry’s 32.7% fall over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cerner Corporation (CERN) : Free Stock Analysis Report

Masimo Corporation (MASI) : Free Stock Analysis Report

AMN Healthcare Services Inc (AMN) : Free Stock Analysis Report

Catalent, Inc. (CTLT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research