Yahoo Finance

Yahoo Finance Investors in Harmoney (ASX:HMY) have unfortunately lost 22% over the last year

The simplest way to benefit from a rising market is to buy an index fund. Active investors aim to buy stocks that vastly outperform the market - but in the process, they risk under-performance. Unfortunately the Harmoney Corp Limited (ASX:HMY) share price slid 22% over twelve months. That falls noticeably short of the market return of around 5.3%. Harmoney may have better days ahead, of course; we've only looked at a one year period. Furthermore, it's down 20% in about a quarter. That's not much fun for holders.

Since shareholders are down over the longer term, lets look at the underlying fundamentals over the that time and see if they've been consistent with returns.

Check out our latest analysis for Harmoney

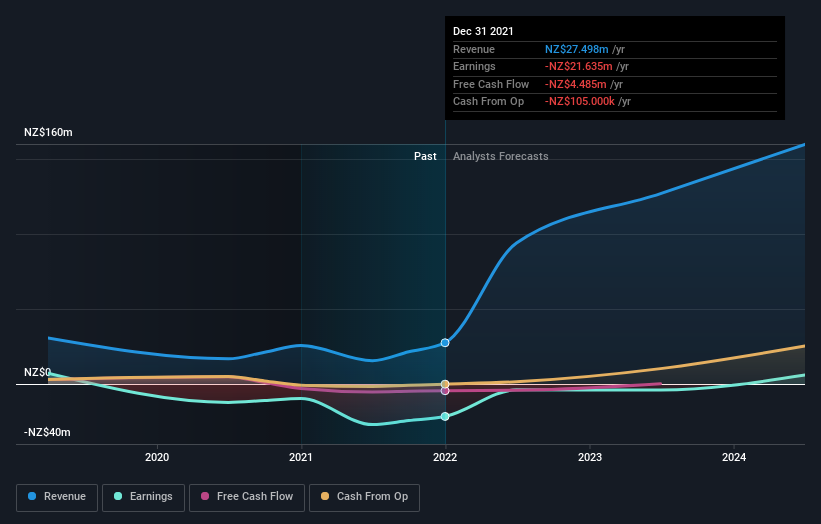

Given that Harmoney didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. When a company doesn't make profits, we'd generally expect to see good revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

Harmoney grew its revenue by 7.0% over the last year. That's not a very high growth rate considering it doesn't make profits. Given this lacklustre revenue growth, the share price drop of 22% seems pretty appropriate. It's important not to lose sight of the fact that profitless companies must grow. So remember, if you buy a profitless company then you risk being a profitless investor.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. So it makes a lot of sense to check out what analysts think Harmoney will earn in the future (free profit forecasts).

A Different Perspective

Given that the market gained 5.3% in the last year, Harmoney shareholders might be miffed that they lost 22%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. With the stock down 20% over the last three months, the market doesn't seem to believe that the company has solved all its problems. Given the relatively short history of this stock, we'd remain pretty wary until we see some strong business performance. It's always interesting to track share price performance over the longer term. But to understand Harmoney better, we need to consider many other factors. Take risks, for example - Harmoney has 2 warning signs we think you should be aware of.

Harmoney is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.