Yahoo Finance

Yahoo Finance New dots, new ranges, new forecasts — Your complete Fed meeting preview

For the seventh time since the financial crisis, the Federal Reserve is expected to raise interest rates on Wednesday.

Economists expect the central bank will lift the target range for its benchmark interest rate by another 25 basis points to a new corridor of 1.75%-2%.

The Fed will release its policy statement along with an updated set of economic forecasts from Fed officials at 2:00 p.m. ET. A press conference with Fed chair Jerome Powell will follow at 2:30 p.m. ET.

Since the Fed raised interest at its March meeting, the unemployment rate has dropped a further 0.3% to a 48-year low of 3.755% while the economy has added 537,000 jobs over that period.

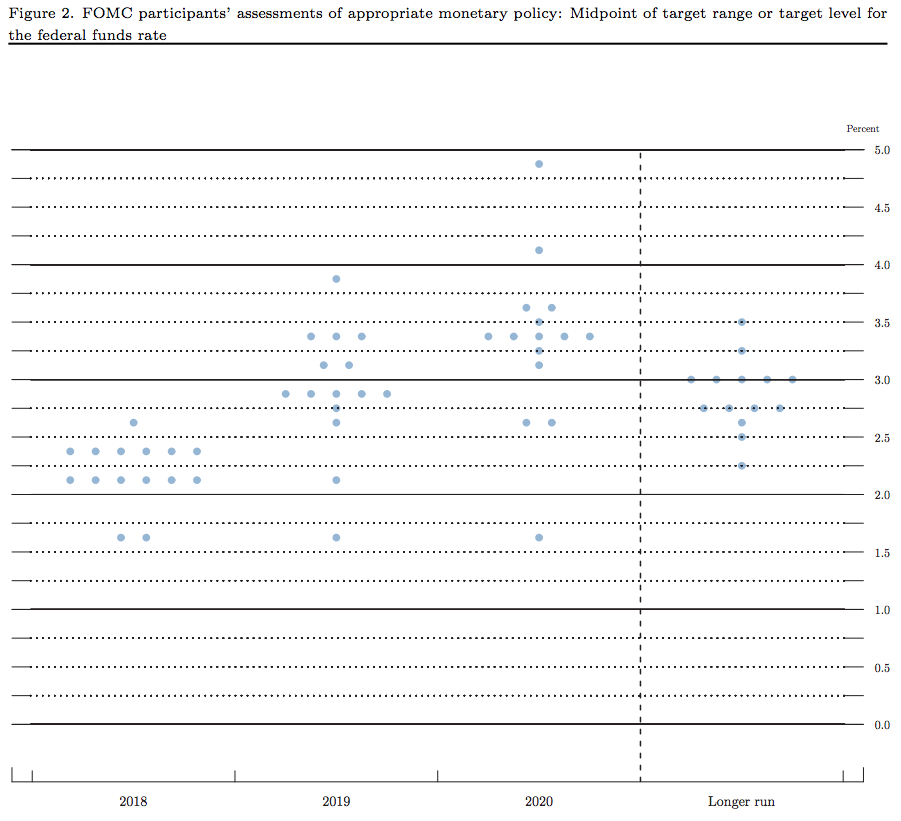

With a rate hike on Wednesday all but assured, markets will be closely watching the Fed’s updated economic projections which include the “dot plot,” a table that shows future interest rate expectations from Fed officials.

In March, the dot plot showed that Fed officials were roughly split on whether two or three additional rate hikes in 2018 would be warranted.

“We expect hawkish changes to the dot plot despite an unchanged Committee composition,” wrote economists at Goldman Sachs in a note ahead of the meeting.

“On net, remarks by Fed officials continued to evolve in a hawkish direction during the spring — most recently those by San Francisco Fed President John Williams after the May employment report. Taken together, we expect the dots will show a four-hike baseline for 2018, up from three at the March meeting.”

According to data from the CME Group, market pricing suggests traders are split on whether the Fed will raise rates three or four times this year.

And whether or not the Fed’s dot plot signals an additional one or two interest rate hikes this year, Michael Feroli at JP Morgan said the policy statement is likely to drop one its signature sentences — “the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run.”

The economic outlook

In March, the Fed responded to the Trump tax cuts.

After having forecast GDP growth in 2018 and 2019 to be 2.5% and 2.1%, respectively, back in December 2017, the passage of the Trump tax cuts just before year-end saw the Fed’s median forecasts for GDP growth this year and next increase to 2.7% and 2.4%.

These forecasts are not expected to be significantly revised on Wednesday. We’d also expect Powell to echo his statements back in March which sought to downplay the significance of these forecasts. “I think, like any set of forecasts, those forecasts will change over time,” Powell said. “And they’ll change depending on the way the outlook for the economy changes. It could change up, it could change down.”

“Economic developments since the March meeting are unlikely to have prompted a major revision to the Summary of Economic Projections,” Feroli said. “Dollar strength and foreign growth disappointments may shave a tick off the 2019 GDP outlook, currently 2.4%, but their current year growth forecast of 2.7% will probably go unrevised.”

Economists at Goldman Sachs expect the Fed’s actual policy statement to indicate an economy that is still on solid footing.

“We expect the FOMC statement to retain the upbeat tone of recent meetings — with an upgrade to household spending, an acknowledgement of lower unemployment, and a hawkish rewording of the forward guidance,” said Goldman Sachs economists in a note to clients ahead of the meeting. “For economic activity as a whole, we expect the ‘moderate’ adjective to remain (both for current and expected growth), as the most likely alternative ‘solid’ is generally reserved for growth in excess of 3%.”

Federal Reserve Chairman Jerome Powell speaks following the Federal Open Market Committee meeting in Washington. (AP Photo/Carolyn Kaster)

In both its March and May policy statements, the Fed said, “economic activity has been rising at a moderate rate.”

Goldman adds, however, that the Fed could acknowledge the recent political turbulence in Italy which roiled markets late last month as a potential risk to the global economic outlook.

“On the negative side, with Italian sovereign spreads returning to levels last seen in the European debt crisis, we think the statement will probably include a subtle reference to heightened uncertainty abroad, echoing recent comments from Governor [Lael] Brainard,” Goldman said.

In a May 31 speech, Brainard said, “recent developments abroad suggest some risk to the downside. Global growth has been synchronized over the past year, but recent developments pose some risk. Political developments in Italy have reintroduced some risk, and financial conditions in the euro area have worsened somewhat in response.”

Brainard also acknowledged recent pressures in emerging markets and trade tensions, adding, “An environment with a strengthening dollar, rising energy prices, and the possibility of rising rates raises the risks of capital flow reversals in some emerging markets that have seen increased borrowing from abroad. Although stresses have been contained to a few vulnerable countries so far, the risk of a broader pullback bears watching. In addition, uncertainty over trade clouds the horizon. An escalation in measures and countermeasures — although an outside risk — could prove disruptive at home and abroad.”

A technical adjustment

Wednesday’s policy decision from the Fed could also have a technical wrinkle that could throw some unsuspecting market observers for a loop.

Since the financial crisis, the Fed has set a 25 basis point target range for the Fed Funds rate with the rate paid for overnight reverse repurchase agreements (ON-RRPs) acting as the floor and the the interest on excess reserves (IOER) it pays to depository institutions serving as the ceiling.

Currently, that range is 1.5%-1.75%. The effective Fed Funds rate — which would expected to be around 1.63% — has been right at 1.7% since the March rate hike, just 5 basis points below the Fed’s targeted ceiling.

To correct this skew towards the upper-bound of its target range, the Fed is expected to increase the interest on excess reserves rate just 20 basis points. This would tighten the spread between RRP and IOER to 1.75%-1.95% while the Fed Funds corridor would still be 1.75%-2%. If current market conditions prevail in the months ahead, this would set the effective Fed Funds rate at 1.9%.

In a note last month, strategists at Deutsche Bank chalked up this tightening of the IOER rate and the effective Fed Funds rate to a number of potential factors.

“Since last December, the effective fed funds rate has been drifting higher inside its 25bp-wide target range, and it currently sits just 5bp below the upper bound,” the firm wrote.

“This is blamed on a number of factors, including higher repo costs after the Treasury had drastically increased its supply earlier this year, the steady decline in supply of bank excess reserves as a result of the Fed’s balance sheet unwind, and the potential elimination of FDIC fees later this year. (The last point may not have had a direct impact on the recent FF-IOER tightening but is a catalyst for further spread compression later this year.)”

Joe Song, an economist at Bank of America Merrill Lynch, wrote in a note to clients ahead of the report that at Chair Powell’s press conference on Wednesday, he is “likely to explain the technical changes to IOER being 5bps lower than the top of the fed funds range. He is likely to explain that this is a one-off adjustment and does not imply a shift in the broader stance of monetary policy.”

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland