Yahoo Finance

Yahoo Finance REA Group Limited's (ASX:REA) Stock Is Rallying But Financials Look Ambiguous: Will The Momentum Continue?

REA Group's's (ASX:REA) stock is up by a considerable 40% over the past three months. But the company's key financial indicators appear to be differing across the board and that makes us question whether or not the company's current share price momentum can be maintained. In this article, we decided to focus on REA Group's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for REA Group

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for REA Group is:

26% = AU$251m ÷ AU$979m (Based on the trailing twelve months to December 2019).

The 'return' refers to a company's earnings over the last year. So, this means that for every A$1 of its shareholder's investments, the company generates a profit of A$0.26.

Why Is ROE Important For Earnings Growth?

So far, we've learnt that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

REA Group's Earnings Growth And 26% ROE

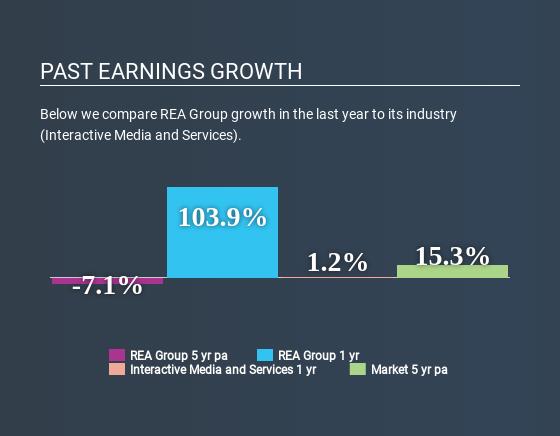

Firstly, we acknowledge that REA Group has a significantly high ROE. Additionally, the company's ROE is higher compared to the industry average of 12% which is quite remarkable. As you might expect, the 7.1% net income decline reported by REA Group doesn't bode well with us. So, there might be some other aspects that could explain this. These include low earnings retention or poor allocation of capital.

With the industry earnings declining at a rate of 7.1% in the same period, we deduce that both the company and the industry are shrinking at the same rate.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Is REA Group fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is REA Group Efficiently Re-investing Its Profits?

REA Group's high three-year median payout ratio of 124% suggests that the company is depleting its resources to keep up its dividend payments, and this shows in its shrinking earnings. Paying a dividend higher than reported profits is not a sustainable move.

Additionally, REA Group has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 51% over the next three years. The fact that the company's ROE is expected to rise to 34% over the same period is explained by the drop in the payout ratio.

Summary

In total, we're a bit ambivalent about REA Group's performance. In spite of the high ROE, the company has failed to see growth in its earnings due to it paying out most of its profits as dividend, with almost nothing left to invest into its own business. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.