Yahoo Finance

Yahoo Finance Recent 12% pullback isn't enough to hurt long-term Antero Resources (NYSE:AR) shareholders, they're still up 306% over 3 years

It's been a soft week for Antero Resources Corporation (NYSE:AR) shares, which are down 12%. But over the last three years the stock has shone bright like a diamond. Over that time, we've been excited to watch the share price climb an impressive 306%. Arguably, the recent fall is to be expected after such a strong rise. The only way to form a view of whether the current price is justified is to consider the merits of the business itself.

In light of the stock dropping 12% in the past week, we want to investigate the longer term story, and see if fundamentals have been the driver of the company's positive three-year return.

Check out our latest analysis for Antero Resources

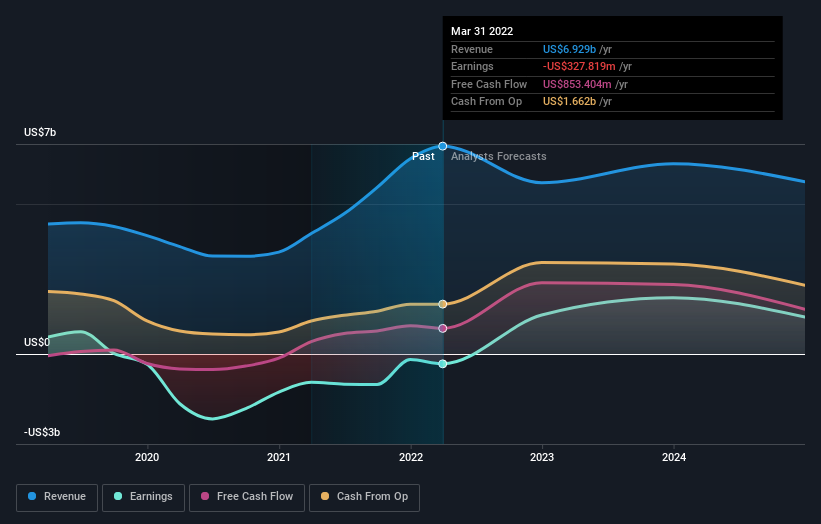

Because Antero Resources made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

Over the last three years Antero Resources has grown its revenue at 17% annually. That's pretty nice growth. Some shareholders might think that the share price rise of 60% per year is a lucky result, considering the level of revenue growth. After a price rise like that many will have the business, and plenty of them will be wondering whether the price moved too high, too fast.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. So it makes a lot of sense to check out what analysts think Antero Resources will earn in the future (free profit forecasts).

A Different Perspective

We're pleased to report that Antero Resources shareholders have received a total shareholder return of 185% over one year. That's better than the annualised return of 9% over half a decade, implying that the company is doing better recently. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Antero Resources , and understanding them should be part of your investment process.

But note: Antero Resources may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.