Yahoo Finance

Yahoo Finance Results: Rockwell Automation, Inc. Exceeded Expectations And The Consensus Has Updated Its Estimates

Rockwell Automation, Inc. (NYSE:ROK) investors will be delighted, with the company turning in some strong numbers with its latest results. Rockwell Automation beat earnings, with revenues hitting US$2.1b, ahead of expectations, and statutory earnings per share outperforming analyst reckonings by a solid 15%. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for Rockwell Automation

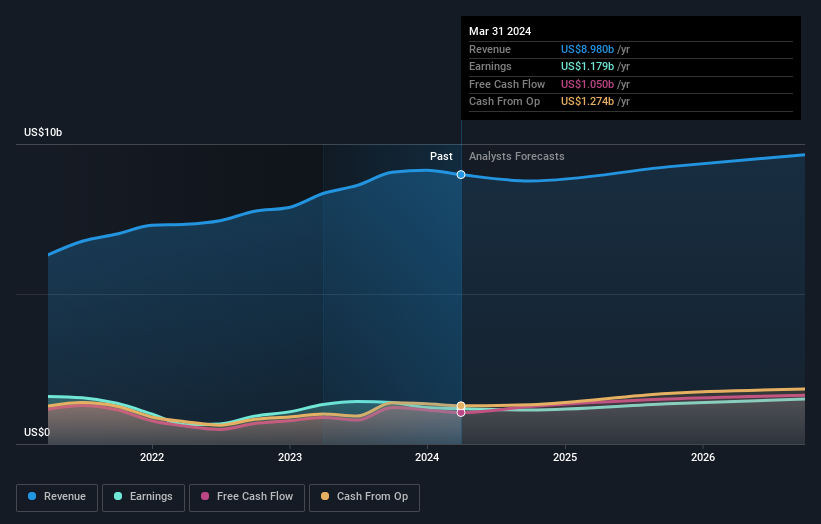

Taking into account the latest results, the current consensus, from the 22 analysts covering Rockwell Automation, is for revenues of US$8.77b in 2024. This implies a perceptible 2.4% reduction in Rockwell Automation's revenue over the past 12 months. Statutory earnings per share are forecast to dip 3.7% to US$9.96 in the same period. In the lead-up to this report, the analysts had been modelling revenues of US$9.11b and earnings per share (EPS) of US$11.23 in 2024. From this we can that sentiment has definitely become more bearish after the latest results, leading to lower revenue forecasts and a substantial drop in earnings per share estimates.

Despite the cuts to forecast earnings, there was no real change to the US$288 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Rockwell Automation at US$361 per share, while the most bearish prices it at US$220. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 4.7% by the end of 2024. This indicates a significant reduction from annual growth of 7.4% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 7.6% per year. It's pretty clear that Rockwell Automation's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Rockwell Automation. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Rockwell Automation going out to 2026, and you can see them free on our platform here..

Before you take the next step you should know about the 1 warning sign for Rockwell Automation that we have uncovered.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.