Yahoo Finance

Yahoo Finance Ross Stores: A Strong Compounder With Consistently High ROIC

Ross Stores Inc. (NASDAQ:ROST) has been a great stock for long-term shareholders. Its share price has skyrocketed from $7 to $144, delivering return of nearly 2,000%, equivalent to the compounded annual return of 17.20% in the past 20 years. In my view, Ross is fairly valued at the current price and can be considered a good opportunity for long-term investors.

Business model benefits manufacturers and consumers

Ross Stores is the largest off-price retail apparel and home fashion store chain in the U.S., operating 1,764 locations in total. The company has two main brands: Ross Dress for Less and dd's DISCOUNTS. According to the company, shopping at Ross locations can potentially save consumers between 20% and 70% off the normal retail price.

The company's principal strategy has been its off-price buying strategies, taking advantage of the imbalance between manufacturers and retail demand. Most of the merchandise sold at its stores are the product of cancelled orders, overruns, late deliveries and weak sales. Moreover, the majority of its inventory, which accounts to 40% of its total inventory, are packaway merchandise that is often bought opportunistically to be stored for seasonal sale. This strategy allows Ross to offer consumers a wide range of high-quality brands at competitive prices. With this business model, manufacturers can clear out their unsold inventory, while consumers can shop brand new products at significant discounts from the normal retail price.

Many investors might worry about the rise of online shopping and e-commerce could cause Ross' brick-and-mortar business to suffer. However, I do not think e-commerce is a big threat. One of the reasons Ross has been successful is it does not offer online shopping. Rather, the retailer offers consumers the unique experience of treasure hunt shopping and shelf browsing, which could not be replicated by online shopping. Furthermore, e-commerce websites like Amazon incur high costs of shipping and high frequent return rates, which does not make sense to focus on a heavily discounted segment.

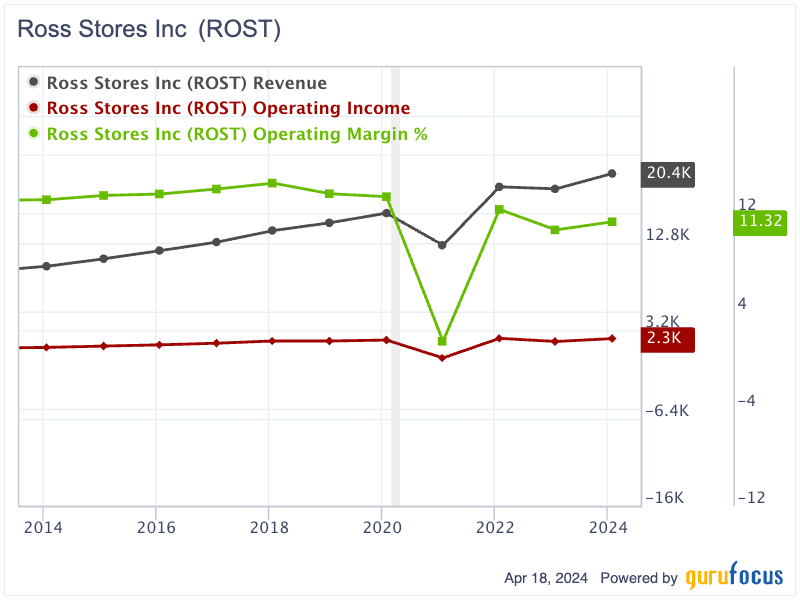

Of the past twenty years, Ross' sales experienced declines in two years, 2020 and 2022. The decline in sales in 2020 was caused by the Covid-19 pandemic, while the 2022 drop was the result of the accelerating inflationary pressures that reduced consumer demand. When considering the retailer's sales performance over the broader timeline, revenue has been on the rise, growing from $3.92 billion in 2003 to $20.38 billion in 2023, delivering a compounded annual growth rate of 8.60%. Its operating income followed a similar trend, increasing from $373.40 million to $2.30 billion over the same period. The operating margin came in at 12.35%, a bit higher than the company's average 20-year margin of 10.64%.

The current situation with rising interest rates and high inflation has discouraged many consumers from making major purchases. Instead, they are now looking for cheaper shopping options, which always benefits Ross since consumers can save money. Thus, the company reported a decent 7% comparable store sales growth in the fourth quarter 2023 and 5% growth for the whole year. Management expects the growth to continue in 2024. In a statement, Chief Financial Officer Adam Orvos said, "We are encouraged by the sustained sales momentum that began in the second quarter of 2023 and continued through the holiday season."

Its revenue is expected to increase by 2% to 4%, driven by 2% to 3% growth in comparable store sales. The retailer also plans to expand its operations by opening 90 new locations in 2024.

Consistently high ROIC

What I find attractive about Ross is its consistent return on invested capital. In the past 20 years, with the exception of the Covid-19 pandemic in 2020, Ross' ROIC has fluctuated in the range of 21.69% to 59.32%. In 2023, its ROIC settled at 23.33%. The 20-year average ROIC came in at around 35.90%. Compared to other retailers, including TJX Companies (NYSE:TJX) and Burlington Stores (NYSE:BURL), Ross is far more profitable. Its ROIC has been higher than both TJX and Burlington Stores most of the time. In 2023, the ROIC of TJX Companies ranked second with 20.79%, while Burlington Stores had the lowest ROIC of only 6.45%.

The high ROIC demonstrates that Ross' management has allocated its capital (both debt and equity) quite efficiently to profitable investments. This is often a sign of a strong competitive advantage and effective management.

Solid balance sheet

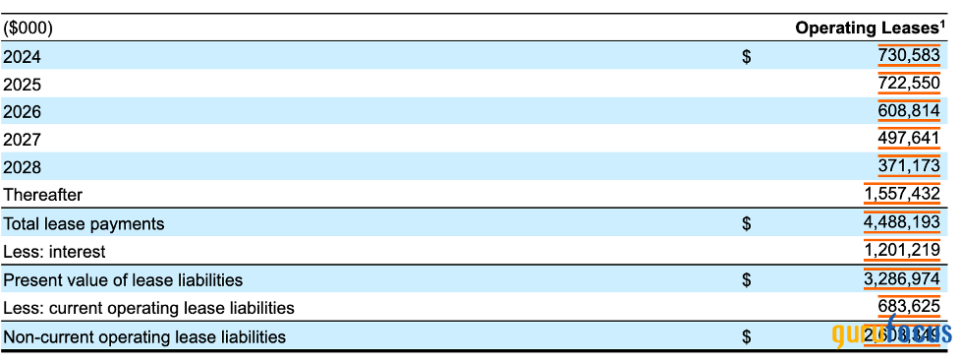

Ross has a quite solid balance sheet with lots of cash reserves. As of February, it held nearly $4.90 billion in cash and cash equivalents, while its interest-bearing debt was only $2.46 billion. As the retailer rents numerous properties for its store operations, it recorded high operating lease liabilities of $3.29 billion. However, the maturities of these leases are spread out over many years, with annual lease payments over the next five years ranging from $371 million to $730.6 million. Given the substantial cash on hand, Ross can easily meet its lease and debt obligations.

Source: Ross' 10-K filing

Dividend payment

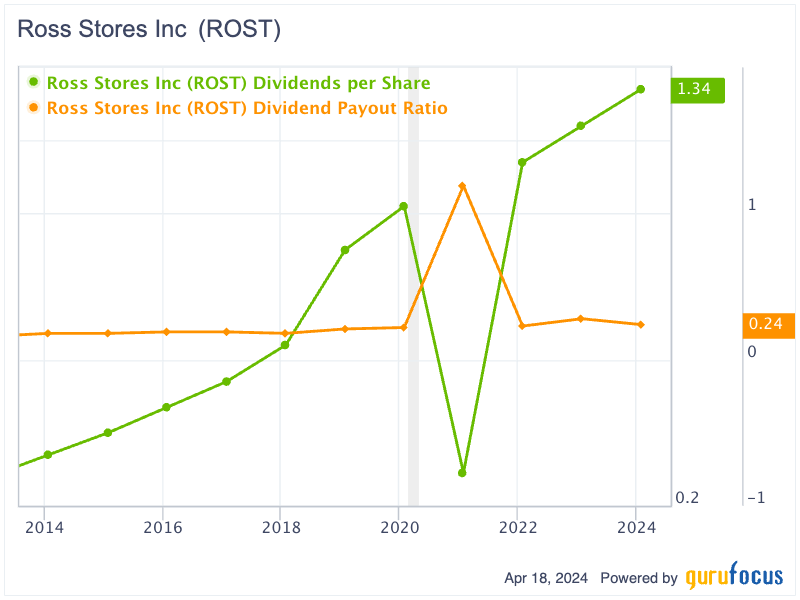

Income investors will love the fact that Ross has been a consistent dividend payer. Since 1994, the retailer has been paying uninterrupted dividends to shareholders. In 2023, the dividend reached $1.34 per share, with a conservative dividend payout ratio of only 0.24. In addition, it spent a lot of money repurchasing shares. In 2023, it spent nearly $247 million to buy back nearly 1.86 million shares. The company has recently also authorized a new two-year $2.10 billion share buyback program. This new share buyback authorization would yield a decent share repurchase return of 4.50% at the current trading price.

Valuation

Ross has an enterprise value-to-Ebit ratio of nearly 19, a bit lower than its own 20-year average earnings multiple of 19.72. The current sales multiple reaches 2.34, higher than the 20-year average sales multiple of 1.55. Thus, the stock appears relatively overvalued from a sales multiple perspective, but fairly valued from an earnings multiple perspective.

If we assume Ross could keep growing its revenue at 8% every single year, its 2028 revenue could reach $30 billion. Applying a current operating margin of 12%, its operating income is estimated to be $3.60 billion. With an earnings yield of 5%, or earnings multiple of 12.50, Ross' enterprise value would reach $72 billion by 2028. Applying a discount rate of 8%, Ross' enterprise value would be worth around $49 billion, just a bit higher than the current enterprise value of $48.30 billion. As a result, I conclude the stock is fairly valued at the moment.

The bottom line

Ross has demonstrated consistent revenue growth, strong cash flow generation and efficient capital allocation with high ROIC. The company's business model, which offers significant savings to consumers, positions it well amidst various macroeconomic conditions.

My analysis shows the stock is fairly valued at the current trading price. As a consistent dividend payer offering a decent share buyback yield and benefiting from current economic conditions favoring discount retailing, Ross Stores stands out as a good opportunity for long-term income investors.

This article first appeared on GuruFocus.