Yahoo Finance

Yahoo Finance Scotts Miracle-Gro vs. Innovative Industrial Properties: Which Is the Better Pot Play?

There's no question about it, marijuana is a very hot topic on Wall Street. With all the hype flying around, you might be tempted to jump aboard and buy a pot stock. However, you don't actually need to do that to gain exposure to the industry and what is expected to be massive growth in demand. Instead, you can buy a supplier to the marijuana industry like The Scotts Miracle-Gro Company (NYSE: SMG) or Innovative Industrial Properties, Inc. (NYSE: IIPR). But which of these two is the better buy?

Aggressive moves

Scotts Miracle-Gro is probably best known for its lawn care products, things like its namesake Miracle-Gro and Roundup. You can buy them at any home improvement store, and they're staples in the lawn care sector. But a few years ago the company stepped back and took a good look at the marijuana space. It was a market Scotts hadn't really focused on, but one that would fit well with its overall strengths.

Image source: Getty Images

Management went on a buying spree. It acquired several companies that were supplying hydroponic gardening products, which have long been used to grow marijuana indoors (even when it wasn't legal to do so). Scotts very quickly established its Hawthorne division, going from effectively zero exposure to marijuana to a run rate of around $600 million in annual revenue from hydroponics. (For reference, the company's trailing 12 months revenue is around $2.6 billion.) It now sells such products to around 1,800 retailers. If pot turns out to be as big as expected, Scotts will likely benefit in a big way.

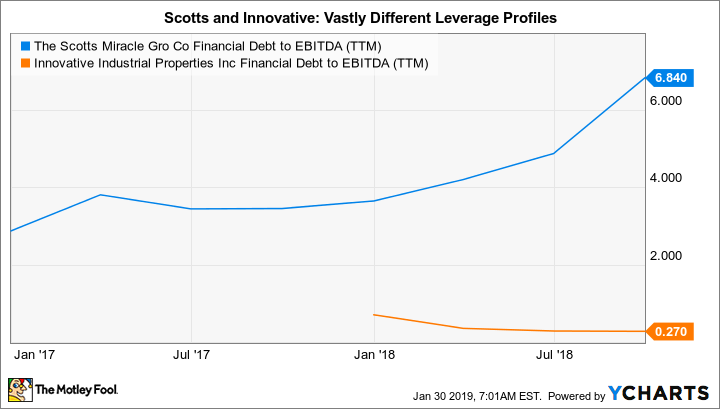

However, the move into hydroponics came at a cost. Long-term debt increased by roughly 50% in fiscal 2018 to around $1.9 billion. Go back a little further and the increase is even more notable: At the end of fiscal 2014, long-term debt was just $700 million. At this point long-term debt makes up nearly 84% of Scotts' capital structure, up from just 55% in 2014. That's a very heavily leveraged balance sheet.

To be fair, the company has been able to handle the increased interest costs in stride. However, Scotts has clearly taken on a big and expensive bet. If it doesn't work out as planned, there could be notable issues -- for example, the company took a one-time charge in fiscal 2018, writing down the value of its Hawthorne business by roughly $95 million. That's not a great sign, suggesting that in management's zeal to expand into a new space it may have overpaid.

They could be used for other things

For conservative investors, Scotts' big bet should be a worry. If the Hawthorne division doesn't live up to expectations there will likely be more one-time charges to come, and all that extra debt will turn into a massive headwind.

That's why more conservative types might want to look at Innovative Industrial Properties. This real estate investment trust, or REIT, owns the facilities in which marijuana is grown.

SMG Financial Debt to EBITDA (TTM) data by YCharts

At the end of 2018 Innovative had 11 buildings in its portfolio covering roughly one million square feet of leasable space. Its properties are 100% leased, with a remaining lease term of over 14 years. As with all REITs, the company generally uses a mix of equity and debt to fund growth. At this point, however, it has made aggressive use of stock sales, and as of the third quarter of 2018 had virtually no debt. And as long as marijuana remains hot on Wall Street it should have little trouble selling more shares to fund its acquisitions.

To be fair, Innovative is tiny, with a market cap of just $500 million or so (Scotts' market cap is over $3.8 billion). And believe it or not, the REIT's dividend yield of 2.2% is a full percentage point lower than Scotts' 3.2% yield. However, with basically no debt and physical assets that could be repurposed if marijuana doesn't take off as expected, Innovative looks like a much lower risk way to play the pot craze.

SMG Dividend Per Share (Quarterly) data by YCharts

It's also worth noting that while the yield is relatively low, dividend growth has been impressive. The first increase was a massive 66% hike in late 2017 (made just three quarters after the company first started paying a dividend), with the second increase in late 2018 tallying a still impressive 40%. That's not surprising for a small REIT, since even modest acquisitions can have a big impact on financial results, which then get passed on to shareholders via a growing dividend. In fact, sometimes the higher yielding stock isn't the better option over the long term.

Big moves, different approaches

When you step back and look at Scotts and Innovative Properties, it's pretty clear that they are both making sizable bets on marijuana industry growth. However, they way in which they are placing these wagers is vastly different. Scotts has levered up its balance sheet in an acquisition binge to create a new division. Leverage can be hugely beneficial, but when times get tough it can also turn into a heavy weight.

Innovative, meanwhile, is focused on partnering with marijuana growers by owning the industrial properties in which pot is grown. It has expanded without the use of debt, and in a worst case scenario can transition the properties to new uses if its marijuana plan doesn't pan out as expected. For more conservative investors, Innovative Properties is an easy win here.

More From The Motley Fool

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool recommends Innovative Industrial Properties. The Motley Fool has a disclosure policy.